TMT Earnings Trade Alert #2

TMT Earnings Trade Alert #2

I take the plunge and buy Oracle ahead of the big earnings release this evening.

Oracle Corporation, based in the United States, generates revenue through a variety of channels, primarily centered around its vast array of software products, cloud services, and hardware.

Here’s an overview of its main revenue generators:

Software Licenses: Oracle sells licenses for a wide range of software products, including database management systems, application servers, and enterprise resource planning (ERP) software. These licenses can be one-time purchases or periodic (annual or multi-year) licenses.

Cloud Services and License Support: A significant portion of Oracle’s revenue comes from cloud services, including Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS). These services provide customers with access to Oracle’s software, platforms, and infrastructure via the internet on a subscription basis. Additionally, Oracle offers support services for its software products, which include updates, security, and customer service. This is a recurring revenue stream that provides a steady income over time.

Hardware: Oracle also sells hardware products, including servers, storage solutions, and network equipment designed to run Oracle software efficiently. This segment includes products from Sun Microsystems, which Oracle acquired in 2010.

Professional Services: Oracle offers consulting, training, and support services to help customers implement and use its products effectively. These services can range from helping businesses integrate Oracle technology into their operations to providing ongoing support and education.

Oracle’s business model locks in customers for long periods through its comprehensive software and hardware ecosystem, support services, and cloud offerings. This model encourages repeat business and generates a steady flow of recurring revenue. Oracle’s push into cloud computing and the transition of its customer base to cloud services have been key drivers of growth, as businesses increasingly move away from on-premises software solutions in favor of cloud-based alternatives.

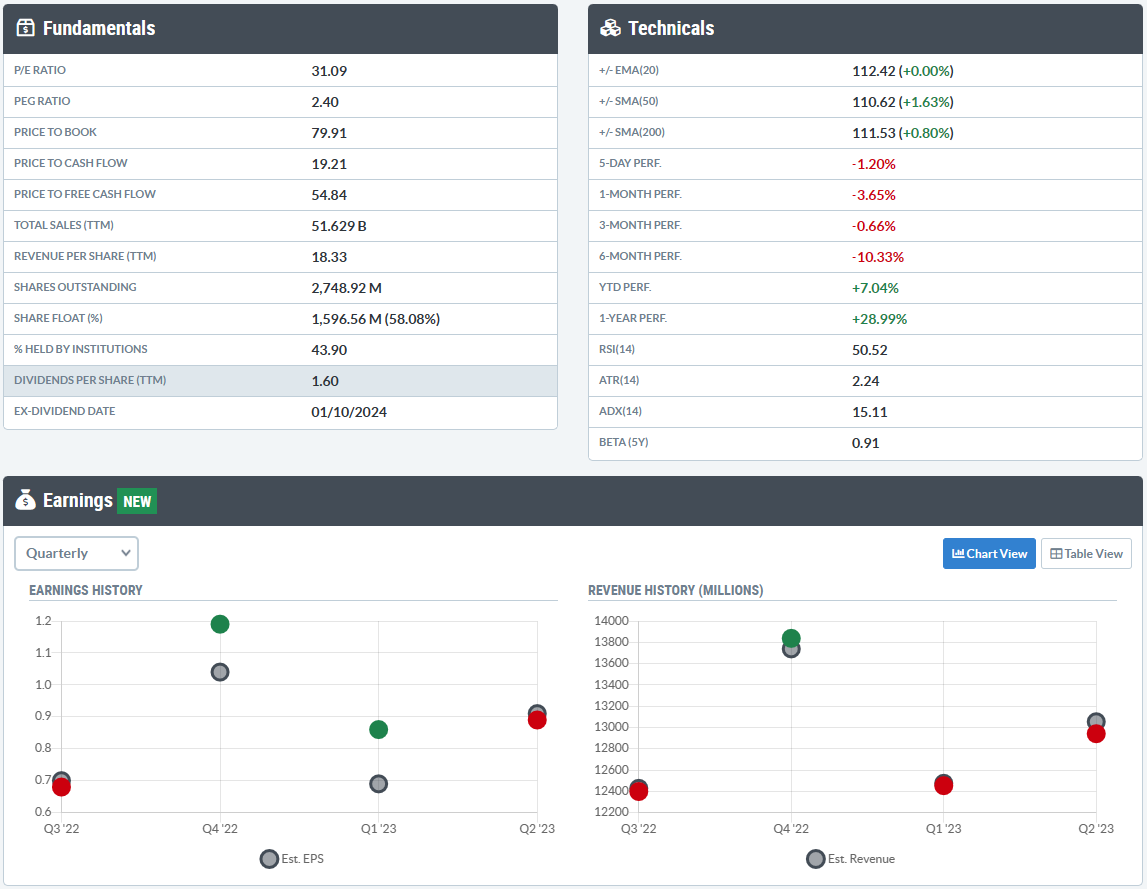

Taking a snapshot of the current fundamental and technical picture we can see Oracle has missed on revenue the last two quarters and for them to miss for a third in a row is rare.

Analysts expect the Austin, Texas-based company to report quarterly earnings at $1.38 per share, up from $1.22 per share in the year-ago period. Oracle is projected to post revenue of $13.31 billion for the latest quarter.

On Dec. 11, Oracle reported upbeat earnings for its second quarter, while sales missed estimates.

UBS analyst Karl Keirstead, who has a Buy rating on Oracle shares, recently inched up his target on the stock to $130, from $125. Ahead of earnings, he checked in with various customers and industry analysts, and found feedback skewed positive, with no material red flags.

Keirstead found that Oracle Cloud Infrastructure, known familiarly as OCI, may be discounting by less than people think against rivals AWS and Azure, and the company has been working around capacity constraints reasonably well as it builds out more data centers.

Cowen analyst Derrick Wood, who maintains an Outperform rating and $130 target price on Oracle shares, says that after two consecutive quarters in which results disappointed the Street, a clean in line quarter would be good enough this time to boost sentiment.

I agree with the statement above and is one reason I think we can get some positive momentum after earnings. Sentiment has been mixed and has a solid chance of flipping to a more positive outlook post earnings.

He thinks OCI will grow 49% in the quarter, just shy of the 50% growth in the November quarter. Wood notes OCI remains Oracle’s key growth driver and finds market trends are becoming more favorable.

Guggenheim Partners analyst John DiFucci maintains a Buy rating and $150 target on Oracle shares, but he has some worries about the February quarter.

He thinks the company will struggle to hit its financial targets given a tough macro backdrop that caused issues in some other software industry earnings reports. But he adds field checks find a robust pipeline and a favorable future.

DiFucci’s advice: Buy the stock on any post-earnings weakness.

Looking at the most accurate analyst ratings going into tonight’s report:

Piper Sandler analyst Brent Bracelin maintained an Overweight rating and cut the price target from $125 to $122 on Jan. 2, 2024.

Erste Group analyst Hans Engel downgraded the stock from Buy to Hold on Dec. 22, 2023.

Morgan Stanley analyst Keith Weiss maintained an Equal-Weight rating and cut the price target from $107 to $106 on Dec. 12, 2023.

Wolfe Research analyst Alex Zukin maintained an Outperform rating and slashed the price target from $140 to $130 on Dec. 12, 2023.

BMO Capital analyst Keith Bachman maintained a Market Perform rating and slashed the price target from $130 to $126 on Dec. 12, 2023.

- Thoughts -

So there was a slew of earnings revisions made after their last earnings report on December 13th. The price action last earnings report was negative where the stock saw an almost 15% fall after these results to the $100 level. Over the coming months, the stock rebounded to roughly where it was prior to the last earnings report ($110-$115). The weakness last earnings report, and a wait and see approach here by many analysts has created a potential gap in sentiment to trade. Before the last earnings report, there were high expectations, but now they have been moderated and are more mixed. This is one reason I like this setup going into tonight’s earnings report.

Most generative AI offerings will are being hosted by Oracles Cloud Infrastructure business, or OCI for short, and will be closely watched this evening. In the previous earnings report, Oracle founder Larry Elision talked about AI bringing a “Gold Rush” for technology spending in the cloud. Now keep in mind we have seen a vigorous growth in their OCI business, but it has slowed for the second straight quarter, and this has given many analysts and investors a reason to pause.

Oracles OCI offering is still growing at a fast clip, but we had seen some deceleration in growth over the last few quarters. Growth has slowed from 76% in the May quarter to 66% in August, followed by 52% in the November period. So, the growth rate will again be a major focus of tonight earning’s release. If they stop the deceleration in growth rates, and they stabilize. The stock should, all things equal, see a positive reaction post earnings.

- Concerns -

Oracle has struggled after its $28 billion acquisition of the healthcare data company Cerner, which was completed in 2022, as it rewrites software to shift its business to the cloud. Issues at Cerner have slowed Oracle’s overall growth rate.

Also, capacity issues have constrained growth. Last quarter Oracle didn’t have enough data centers to meet demand.

Some other concerns have been with Document 79, which targets foreign companies in China that provide software. Two of the last biggest players are Microsoft and Oracle. So, there is an ongoing government-based program to eliminate American companies within China by replacing them with more homegrown offerings.

CPI print will happen at 8:30 tomorrow morning, so this will throw this trade a curveball, though I think it’s a small probability. It’s a risk I’m willing to take.

- The Merciless Trade -

Looking at the daily chart below, we can see that we sold off sharply after the last earnings report. Now three revenue misses in a row are rare for Oracle. While it surely can happen, I like the mixed sentiment going into this report. The markets should react positively to any upside surprises on EPS and revenues. The stock has been hugging the 50-day and 200-day SMA over the last few weeks. As the company has continued to underperform the S&P 500 mightily since September of last year. After the earnings report is released tonight, Oracle's relative performance could move higher.

Looking at the trades, I have been throwing around two different bull call spreads and have decided on one of them after careful thought. One was pretty aggressive, and the other trade was expecting little movement post earnings. I have gone with the former, looking for a breakout above $118 post earnings. Now, on the downside, I feel good, as the best odds I believe are for a breakdown move to the $100 level not occurring again this quarter. So that’s why I was looking for trades just to take advantage of the option premiums. I even thought about buying the stock outright and selling options for that reason. Now that being said, if they really disappoint, missing on revenue with a poor outlook. This stock could surely move back to $100 post earnings. This I put at around a 20% chance of occurring.

The highest odds, I believe, are in the stock trading plus or minus 5% post earnings, trading roughly in-between $107-$117. While I feel there are slightly less chance, we rally up 10% plus post earnings. This market climate is conducive to these big moves. So, because of the current equity climate, I have taken a trade based on the thesis of a breakout over $118 post earnings.

For that reason, I bought the April 19th $110 for an estimated $7.30 and selling the April 19th $130 calls for an estimated $1.30.

This trade is a Bull Call Spread April 19th $110/$130 on ORCL.

Created by buying the April 19th calls for $7.30.

And

Sell an equal quantity of $130 calls for April 19th against your $110 calls.

Creating a trade that cost and has a max loss of $6.00 per contract.

Max gain would be $14.00 a contract if this trade was held to expiration and was at or over $130 on the close on April 19th.

The company and the equity markets are relatively strong and in a bullish run, but I won’t be holding this trade for a few months. At best, I will hold it a week or two if I felt I had a strong chance of a capturing the move that didn’t happen after earnings.

If Oracle moves toward $120-$125 post earnings, I will look to exit withing a few days, if not tomorrow.

On the downside, if we breakdown under $105 in a serious, sustained manor after earnings, I will sell for a loss and move on.

- Conclusion -

Oracle is up against the biggest in the cloud industry with AWS and Microsoft’s Azure, but they do integrate within these ecosystems as customers are able to run Oracle Database on OCI inside Azure. Also, with the rapid growth in cloud in Oracles offerings and the surge in AI spending. I would take the bet that Oracle handily beats on revenue this evening even within a tough operating environment.

This trade isn’t for those who can’t afford losing it all. That being said I did go out over a month to create a situation where losses should be around 70%-80% in most worst-case scenarios and with a breakout move to around $125 we should see gains around 100%.

Well, that’s it for today’s TMT Earnings Trade Alert. I hope you enjoyed a bit of a dive into my process of trading these binary events.

Have a great week. Be good.

Eric

Good call.

Good luck and hope this trade pays out!